When it comes to collecting business debts, it is important to choose the right debt collection service for your organization. Thomas J. Maccari, P.A. is a commercial debt collection agency in Florida that offers a full suite of debt collection…

When it comes to collecting business debts, it is important to choose the right debt collection service for your organization. Thomas J. Maccari, P.A. is a commercial debt collection agency in Florida that offers a full suite of debt collection…

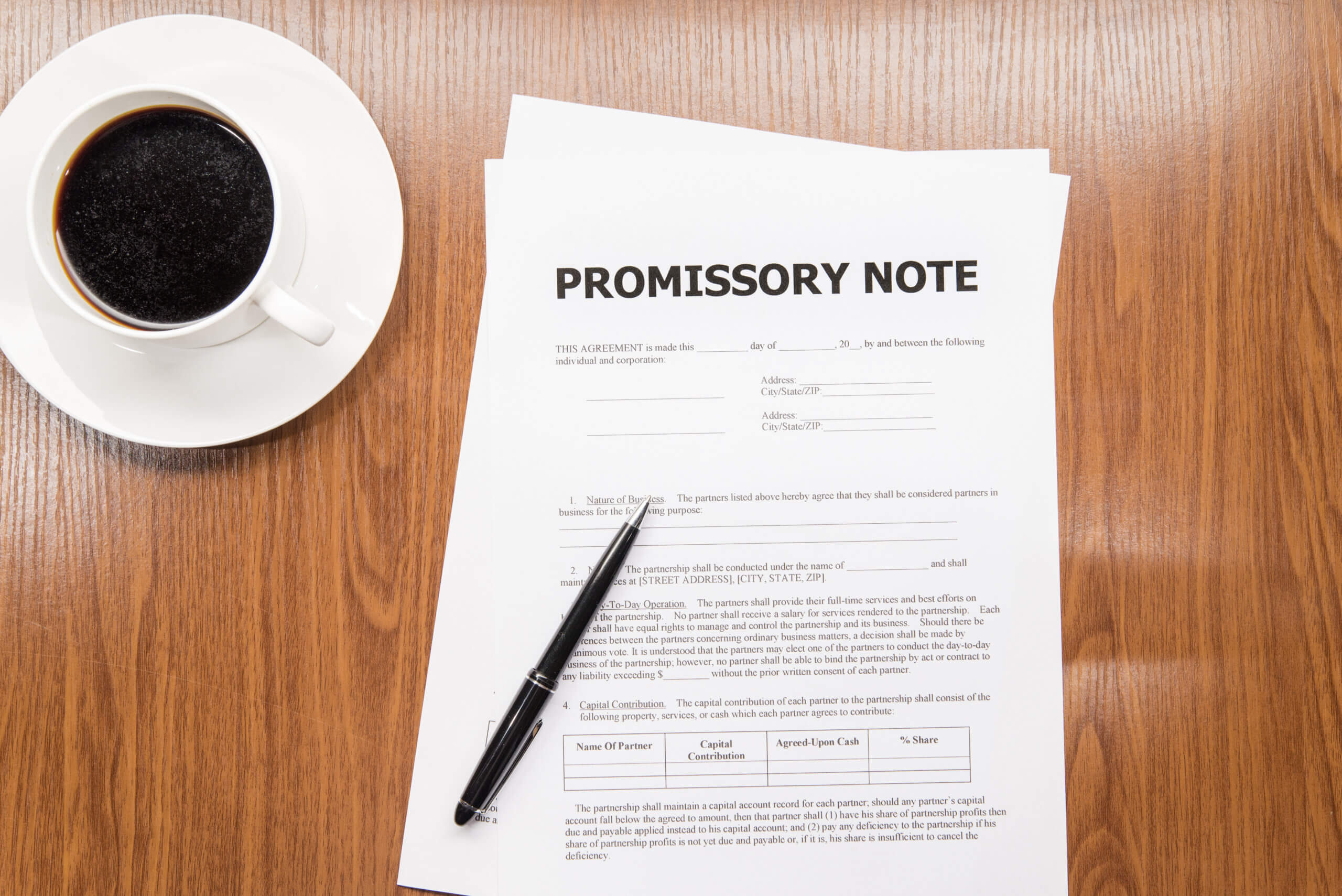

A promissory note is a legally binding document that outlines the terms of a loan or other debt agreement between two parties. It serves as a written record of the agreement and can be used as evidence in court if…

They are often considered a part of the legal world and are used for various other contractual agreements. However, understanding what they mean, how they work, and if they’re right for you can be tricky. This blog post will provide…

Thousands of Americans are contacted by commercial collection companies each year in an attempt to collect a debt. Some of these commercial collection services can be downright ruthless in their attempt to collect money, leaving you stressed and anxious at…

The perfect solution to your cash-flow issues may not exist. Commercial lien and debt collection services can be a double-edged sword. While they can help you get the most out of your money, they can also bring negative consequences. By…

Businesses face the challenges of collecting from vendors that owe them money or products and services. The challenge is that most collection attorneys are focusing only on the consumer side of things. According to the Collection Bureau of America, commercial…

Debt collectors work for creditors to collect debts owed by consumers. They often contact people who owe money via phone calls, letters, and even text messages. If you owe money, you may receive a collection notice from a creditor. Additionally,…

Construction is a difficult industry. Surviving includes a significant work ethic, excellent problem-solving abilities, and a commitment to client service. Most contractors would tell you that it’s all worth it to make their customers’ dreams a reality. It’s even wonderful…

Businesses are not required to hire a commercial collections lawyer in Delray Beach to draft their contracts. However, it is important to note that if money is involved, you risk a substantial loss by not having a lawyer at your…

A construction lien, also known as a mechanic’s lien, is a strong and legal way for contractors to get paid for services or materials they provide on a project. It is a claim filed by workers who have completed work…